Buying a home is one of the most significant financial decisions most people will ever make. Before signing any paperwork, it is essential to understand exactly what your monthly mortgage payment will be — and what factors influence it. Knowing how to calculate mortgage payments gives you the power to compare loan options, negotiate better terms, and plan your budget with confidence.

What Makes Up a Mortgage Payment?

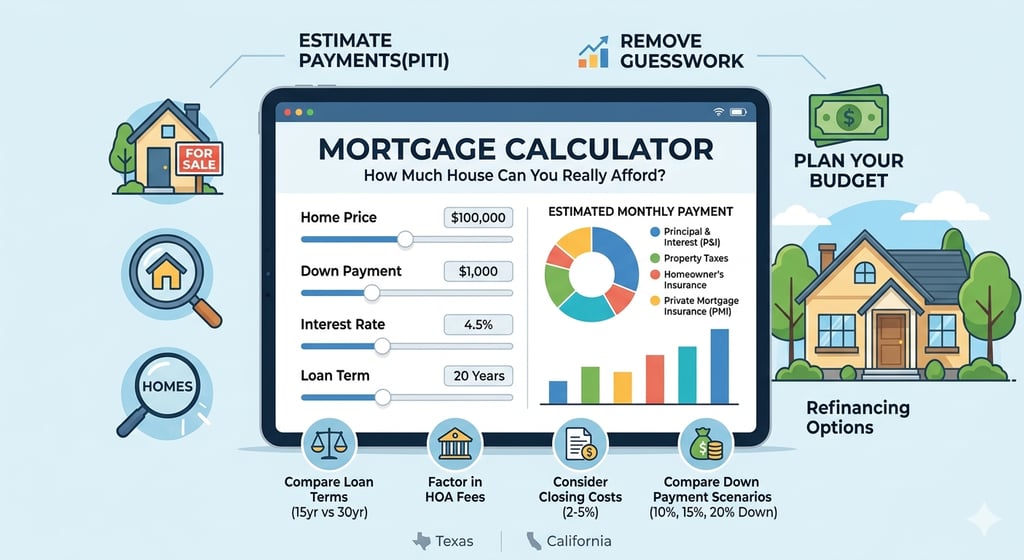

A monthly mortgage payment typically consists of four main components, often abbreviated as PITI:

⦁ Principal — The portion that reduces your loan balance

⦁ Interest — The cost of borrowing money from the lender

⦁ Taxes — Property taxes collected and held in escrow

⦁ Insurance — Homeowners insurance, and PMI if applicable

For simplicity, most mortgage calculators focus on principal and interest (P&I). Taxes and insurance vary by location and policy.

The Mortgage Payment Formula

The standard formula for calculating monthly mortgage payments (principal + interest) is:

M = P × [r(1 + r)^n] / [(1 + r)^n - 1]

Where: M = monthly payment | P = principal loan amount | r = monthly interest rate (annual rate ÷ 12) | n = total number of payments (loan term in years × 12)

Example Calculation

Say you borrow $350,000 at a 6.5% annual interest rate for 30 years:

⦁ r = 6.5% ÷ 12 = 0.5417% per month = 0.005417

⦁ n = 30 × 12 = 360 payments

⦁ M = 350,000 × [0.005417 × (1.005417)^360] / [(1.005417)^360 - 1]

⦁ M ≈ $2,212 per month (principal + interest)

Over 30 years, you would pay approximately $796,320 total — meaning you pay about $446,320 in interest alone.

How Interest Rate Affects Your Payment

Even a small change in interest rate has a dramatic effect on your payment and total cost. For a $350,000 loan over 30 years:

⦁ At 5.0% — Monthly payment: $1,879 | Total paid: $676,440

⦁ At 6.5% — Monthly payment: $2,212 | Total paid: $796,320

⦁ At 7.5% — Monthly payment: $2,447 | Total paid: $880,920

This is why shopping for the lowest possible interest rate is so important.

15-Year vs. 30-Year Mortgage

Choosing between a 15-year and 30-year mortgage is a major decision:

15-Year Mortgage: Higher monthly payments but you build equity faster, pay significantly less interest overall, and own your home outright in half the time.

30-Year Mortgage: Lower monthly payments, more cash flow flexibility, but you pay much more interest over the life of the loan.

What Is PMI and When Do You Need It?

Private Mortgage Insurance (PMI) is typically required if your down payment is less than 20% of the home's purchase price. PMI protects the lender — not you — if you default. It typically costs between 0.5% and 1.5% of the loan amount per year, added to your monthly payment.

Once your equity reaches 20%, you can request to have PMI removed.

Conclusion

Calculating your mortgage payment before you shop for a home puts you in the driver's seat. Use the Numovix Mortgage Calculator to explore different loan amounts, interest rates, and terms in seconds — so you can find a payment that fits your budget and your life.